Key points:

- At current immigration levels, the US labor force is projected to shrink by roughly 1.2 million workers by 2040. The near-term decline is sharper: a drop of about 3.7%, or 5.9 million workers, by 2032 – driven in large part by aging and retiring workers, rather than AI-driven change.

- The labor market segments expected to see the biggest declines in employment are also the ones where AI tools are least likely to help compensate for labor shortages. AI’s labor-market impact is expected to be concentrated almost entirely in high-wage, white-collar sectors, where worker shortages will be less of a problem.

- The result will be a growing structural mismatch between where workers are and which jobs need them. Our estimates suggest this will increase the aggregate unemployment rate between 0.5 and 3.5 percentage points by 2040, with unemployment in certain sectors potentially rising by much more.

- The defining labor market challenge ahead is labor reallocation, not creation. Upskilling, credential reform, and better employee-job matching will be the primary levers available to better align the workforce.

By 2040, there could be some 1.2 million fewer workers in the workforce, and as many as 5.6 million fewer jobs, according to a new projection from Hiring Lab. Unemployment could almost double, to near 8%. On their own, those challenges are daunting and represent a clear break from the past 250 years of US economic growth. But there is also opportunity. Our analysis shows there will be plenty of work to do and workers available to do it, but only if the market can find ways to effectively reallocate workers to where they are needed — and away from where they aren’t.

Three structural forces are colliding in the US labor market: an aging workforce and accelerating retirements, a sharp slowdown in immigration, and the rise of AI. Each of these forces alone would represent a major change in the US job market. Taken together, they are expected to drive a growing mismatch between the jobs workers will have (and want), and the jobs the economy will need. Over the next 15 years, that mismatch will build quietly but significantly.

This is not a cyclical story. Cyclical slowdowns are typically resolved through corresponding expansions. Structural mismatches — driven by demographic shifts, reallocation frictions, and technology-driven changes — do not. Addressing them will require deliberate action outside of the standard economic policy toolkit, and the window to act is shorter than it appears.

The supply picture: Fewer workers, sooner than you think

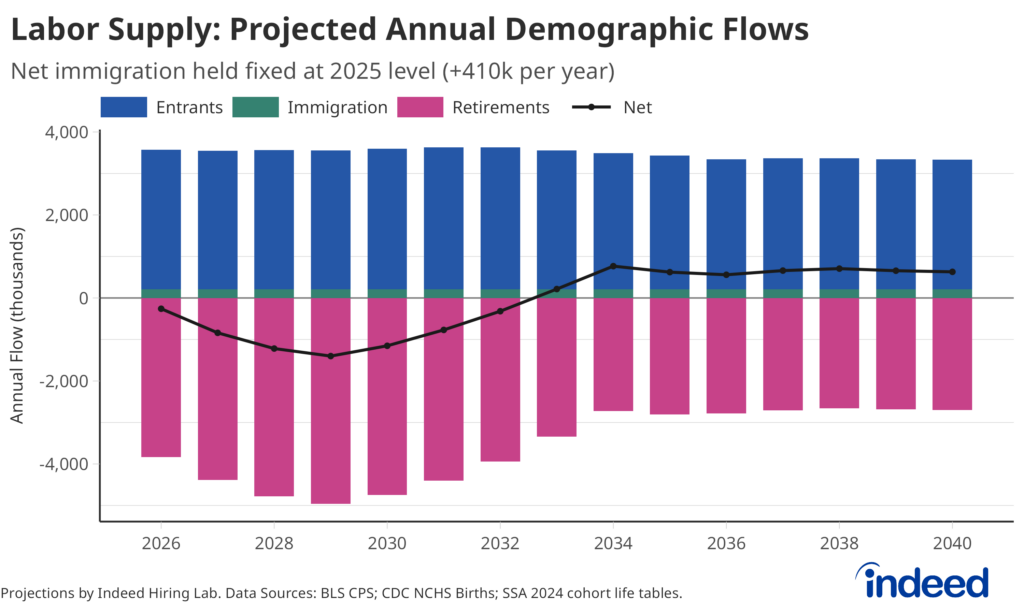

The headline labor force projection looks almost reassuringly modest. In 2025, there were approximately 159.1 million workers in the US labor force across the 10 employment supersectors tracked by the Bureau of Labor Statistics’ Job Openings and Labor Force Turnover Survey (JOLTS). By 2040, the size of this labor force is projected to shrink by roughly 0.7% from 2025 levels, a net decline of about 1.2 million workers. But the trajectory to get there is not linear, and the headline obscures a more significant near-term disruption.

Between 2025 and 2032, the labor force is projected to decline by roughly 3.7%, or some 5.9 million workers, before partially recovering through the back half of the decade. By far the biggest driver of this front-loaded decline in the labor force is the impending retirements of older workers. The youngest Baby Boomers will turn 68 by 2032, at which point the entire generation will be old enough to qualify for full Social Security benefits — a big incentive to enter retirement, if they haven’t already.

At the same time, as more people are expected to leave the market, fewer are expected to enter it. The persistently low fertility rates that have prevailed in recent years will reduce the number of young workers entering the labor market moving forward. Immigration has historically supplied a steady stream of workers to augment native-born entrants, especially in certain labor-intensive sectors such as construction and healthcare. But recently, it has slowed sharply. For this analysis, net migration was held at 410,000 a year, consistent with the reduced levels that prevailed in 2025. Under these conditions, the foreign-born labor force continues to grow, but at a pace far below historical norms.

The result is a labor market aging out at the top faster than it replenishes at the bottom, and doing so unevenly across sectors.

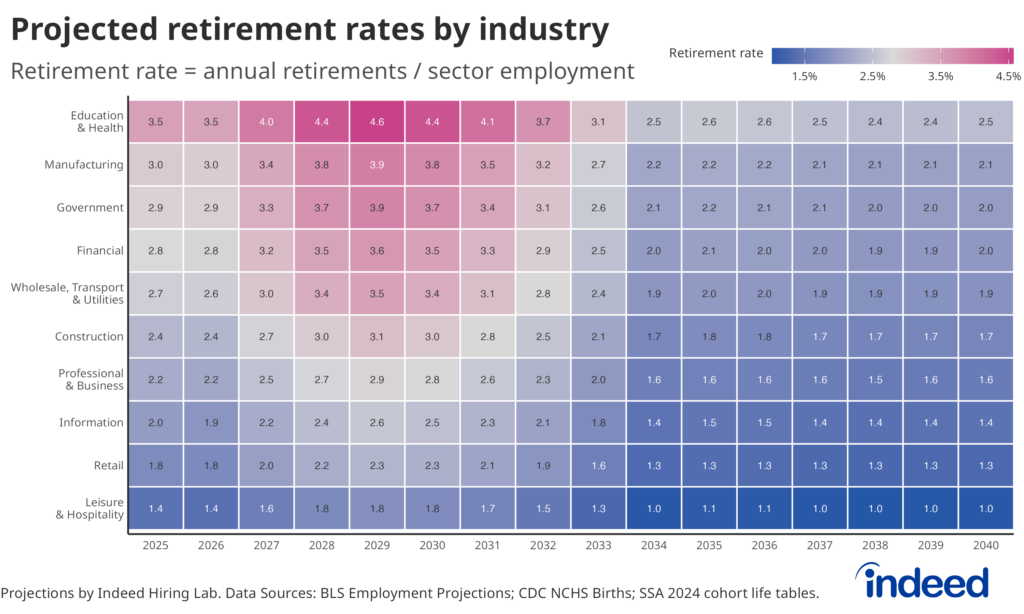

In a handful of sectors that today employ a large share of older workers — including education & health, manufacturing, and government — retirement rates already (or soon will) exceed 3%, well above the rate at which new workers will flow in to replace them. There are several reasons to expect limited replacement rates in some of these industries, including specialized education requirements (healthcare) and generally lower pay (government, manufacturing). Many new labor market entrants, especially college graduates, are likely to continue seeking employment in fields that more closely match their fields of study and/or those they expect to pay more, typically white-collar fields. The result will be a relative abundance of available workers in some sectors, and accelerating shortages in others.

AI won’t fill the gap — at least not where it matters most

AI is already reshaping how work gets done, and its footprint in the labor market will grow considerably over the next 15 years. But its impact is likely to remain uneven: AI will be most transformative in industries that are not facing labor shortages.

To start, AI transmits to the labor market through three channels:

| Channel | Effect |

| Productivity | AI makes workers more productive. The same person gets more done. |

| Replacement | AI replaces specific tasks that humans previously performed. Destroying tasks and jobs. |

| Expansion | AI leads to new tasks where humans have a comparative advantage, creating new jobs and improving others. |

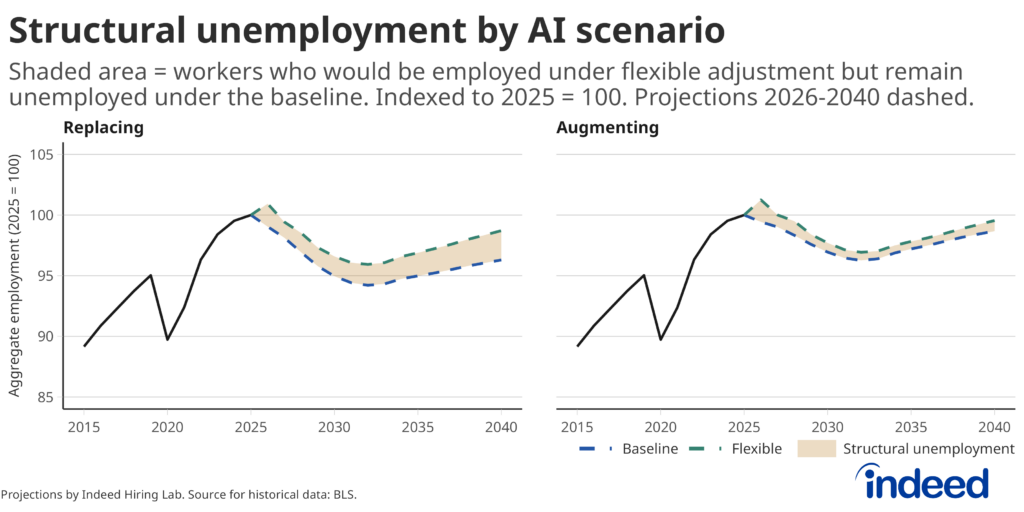

The balance between these channels will determine whether AI is a net positive or negative for employment in any given sector. That balance varies considerably across industries. For this analysis, we consider two scenarios: one in which AI is more likely to replace human labor, and one in which it is more likely to augment human labor rather than replace it.

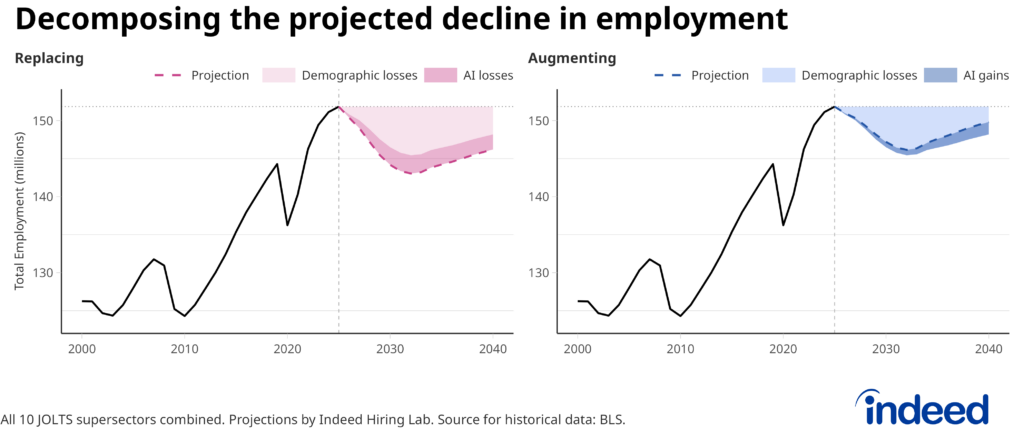

In the replacing scenario, we assume AI’s effect will be largely destructive, eliminating some tasks and destroying some jobs entirely. While AI is also likely to create new tasks and jobs in this scenario, these expansive impacts are secondary. Under the augmenting scenario, task/job destruction is much less frequent, and AI primarily takes on a labor-enhancing role, creating new tasks and jobs and making workers more productive. These scenarios can lead to quite different impacts on the labor market. In the replacement scenario, AI destroys jobs on net and exacerbates some of the demographic challenges described above. In the augmenting scenario, AI plays a limited role in mitigating (though not completely counteracting) some demographic challenges.

In the replacement scenario, employment across the 10 JOLTS supersectors is expected to decline by 8.8 million by 2032, or 5.8%, from 151 million in 2025 to approximately 142.2 million. But even with this more destructive view of AI, 72.7% of the decline through 2032 (6.4 million jobs) is driven by demographic shifts (aging and immigration), while just 27.3% (2.4 million jobs) is driven by AI disruption. By 2040, the overall decline in employment under this scenario (compared to 2025) is expected to be 5.6 million jobs, 64.9% of which is due to demographics and 35.1% to AI.

Even in the more optimistic augmenting scenario, demographics continue to drive overall employment down, even though AI leads to aggregate job gains. In this scenario, new job creation and enhanced productivity offset around 11% of the job losses caused by demographic shifts, and job losses total around 2 million by 2040.

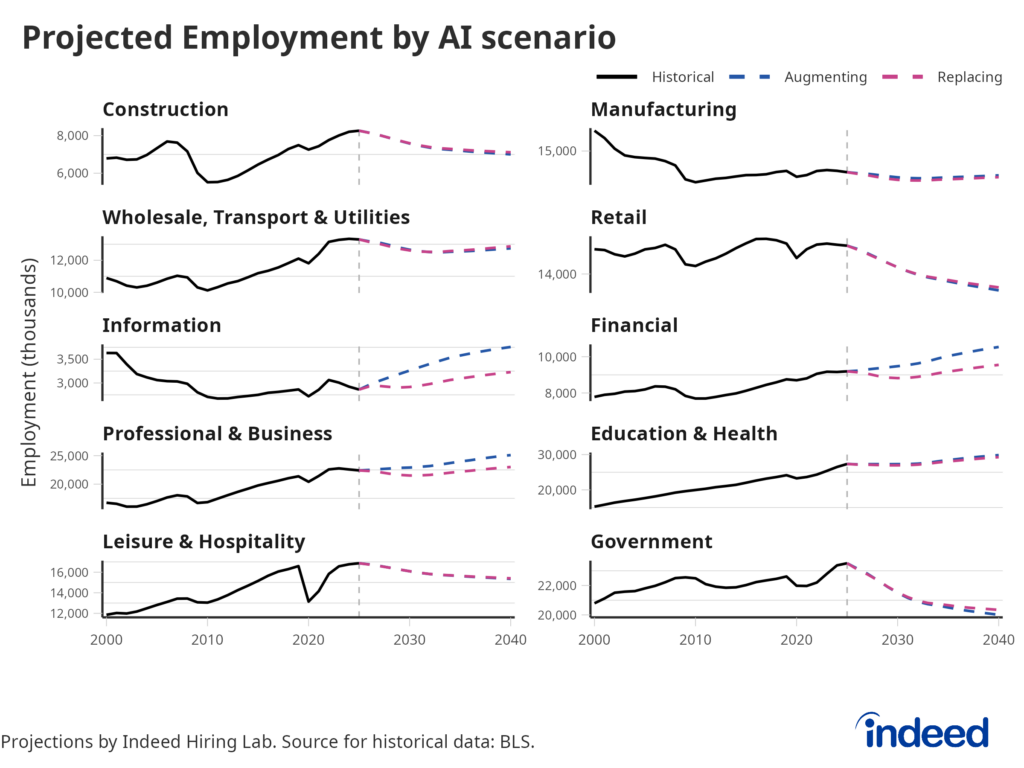

But aggregate shares can be misleading. The sectors most exposed to AI disruption — including information, financial activities, and professional and business services — are the same sectors that tend to attract college graduates and offer above-average wages. These are not expected to be sectors facing acute worker shortages. If anything, they are already well-supplied with entrants eager to work in them. And in a replacing AI scenario, many of those would-be entrants into these fields will likely be left out in the cold. The combined unemployment rate across information, financial activities, and professional and business services rises from 4% in 2025 to 12% by 2032 in the replacing scenario (21.2% in information, 11.8% in financial activities, 10.7% in professional & business services).

The sectors facing the most significant labor shortages – construction, healthcare, government – are precisely the ones where AI offers the least relief. AI has and will destroy some tasks and improve others in these sectors. But in general, healthcare roles require hands-on clinical judgment that AI can’t easily replace; construction requires physical presence and site-specific problem-solving that AI may lack the flexibility for; and government tends to lag other sectors in technological innovation. The model also shows essentially no AI impact in sectors including retail and leisure & hospitality, which tend to attract younger workers, have very few barriers and are minimally exposed to AI disruption. In the replacing scenario, unemployment in many of these sectors is expected to stay below 5% through 2032 (Construction: 4.2; Wholesale/Transportation/Utilities: 4.5%; Retail: 4.0%; Education and Health: 4.9%).

This asymmetry has real consequences for workforce planning. If AI evolves in a more augmenting direction, it could create new roles in exposed white-collar sectors and absorb some of the anticipated oversupply of workers with those skill sets. But if it evolves in a more replacing direction, those same sectors will face a significant glut of structurally unemployed workers with few obvious alternative pathways. Either way, AI does almost nothing to address the shortage problem in the sectors where shortages are most acute.

The reallocation problem is harder than it looks

Even in a world with no AI at all, our model shows that structural unemployment will rise. The reason is friction — the real and substantial difficulty of moving workers between industries, even when demand exists on the other side. It’s not so easy for a worker with tech skills, accustomed to a tech salary, to move from the oversupplied software industry to the undersupplied healthcare industry.

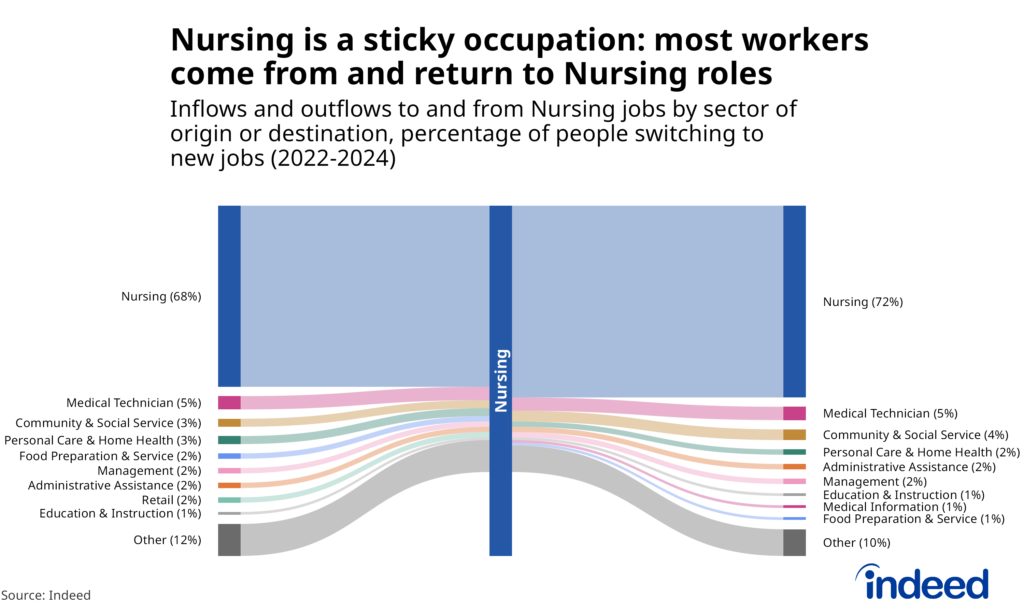

For example, as it stands today, 68% of nurses entered the profession directly from the nursing sector, according to previous Hiring Lab research. And when nurses leave a role, 72% remain in nursing. Those figures are not simply a reflection of preference. They reflect the combination of required credentials, training time, and wage expectations that combine to create a high barrier to entry for the field, and effectively close the pipeline to workers from other fields, even motivated ones.

Our research explicitly incorporates these frictions, accounting for retraining costs, required credentials, wage differentials, and demographic factors that shape who works where. What it reveals is a consistent pattern across industries.

Some sectors are relatively permeable. Professional and business services encompass a wide range of roles with varying educational requirements, and workers can enter from many backgrounds with modest retraining. Other sectors are not. Construction, education and health, and leisure and hospitality all feature high barriers, low wages, or both, limiting inflows even when job openings are strong and demand is clear.

The aggregate effect is a rise in unemployment that is structural, not cyclical. Structural unemployment, driven by a mismatch between worker skills and available jobs rather than by insufficient overall demand, is slower to build and much slower to resolve. Workers in oversupplied sectors will eventually reskill, and wages and/or wage expectations will eventually adjust, but both will take time. In the interim, unemployment will climb. In the AI-replacing scenario, our model projects that overall unemployment could rise by approximately 3.5 percentage points by 2040, from the current 4.3% to something closer to 8%.

Implications for policy and practice

These projections are not fixed. They reflect the trajectory implied by current policy and current levels of labor market friction. Both are changeable.

In our modeling framework, the difference between the baseline scenario (with realistic frictions) and a frictionless counterfactual is the structural unemployment that policy and employer action could, in principle, close. That gap is meaningful; it represents millions of workers who would be employed if reallocation were easier, and who might remain unemployed not because jobs do not exist, but because the pathways to reach them are too costly or too obscure.

Reducing the cost of retraining, through subsidized programs, income support during transitions, or compressed credential pathways, could directly lower friction. Making credentials more portable across states and sectors could reduce information barriers. Wage supports in high-need, lower-wage sectors, including retail and healthcare, could shift the cost-benefit calculation for workers considering a transition.

Employers have a role here that often goes underappreciated. Better labor market matching, using data to surface opportunities workers might not otherwise consider, can help address information frictions that are harder to measure but no less real. The construction firm that cannot fill a supervisor role because credential requirements are outdated is a friction problem. So is the experienced worker in a declining sector who never learned that an adjacent industry is actively hiring people with transferable skills. These are not problems that resolve themselves; they require deliberate attention to how jobs are described, how they are sourced, and who is considered for them.

Looking ahead

The US labor market is entering a period defined less by headline employment numbers and more by the underlying architecture of who works where and how easily they can move. Demographic decline, reduced immigration, and the uneven advance of AI will not produce a single dramatic crisis. They will produce something quieter and, in some ways, harder to address. The result is a slow-building mismatch that compounds over time and shows up not in mass unemployment but in persistent pockets of structural joblessness alongside unfilled vacancies in sectors that badly need workers.

The next 15 years will test whether institutions, employers, and workers can adapt quickly enough to a labor market that does not need more people in aggregate, but rather needs different people in different places. The policy and employer interventions that can make a real difference are not glamorous. They involve retraining, credential reform, better job matching, and sustained attention to the sectors with the most severe shortages. But the payoff, in reduced structural unemployment and a more functional labor market, is significant.

There will be plenty of work to do going forward, and enough people to do it. The defining labor market challenge ahead will be to create new ways of matching the work that needs doing with the people who need to do it.

………………..

Methodology

This analysis draws on modeling of the 10 JOLTS supersectors, starting from a 2025 labor force of 159.11 million and employment of 151.84 million (implying a 4.5% unemployment rate). Farm workers and the self-employed are excluded due to data limitations. Net immigration is held at 2025 levels throughout, and no policy changes are assumed to Social Security, Medicare, TANF, or other programs empirically shown to affect employment decisions.

The size of the working-age population is estimated using native birth rates obtained from the CDC and death rates from the Social Security Administration’s 2024 cohort life tables. Forward projections assume no changes to labor force participation rates for workers aged 64 and below. For workers aged 65-75, we assume a wave of retirements over 2026-2032 that gradually normalizes as baby boomers age out of the workforce.

Labor market dynamics are modeled using a search-and-matching framework, À la Diamond, Mortensen, and Pissarides’ canonical setup. We adjust the standard model to include cross-industry flows, new labor market entrants from immigration and degree completions, endogenous education decisions, gender specific occupational preferences, and AI integration. The model’s fixed parameter values are calibrated using 2024-2025 data.